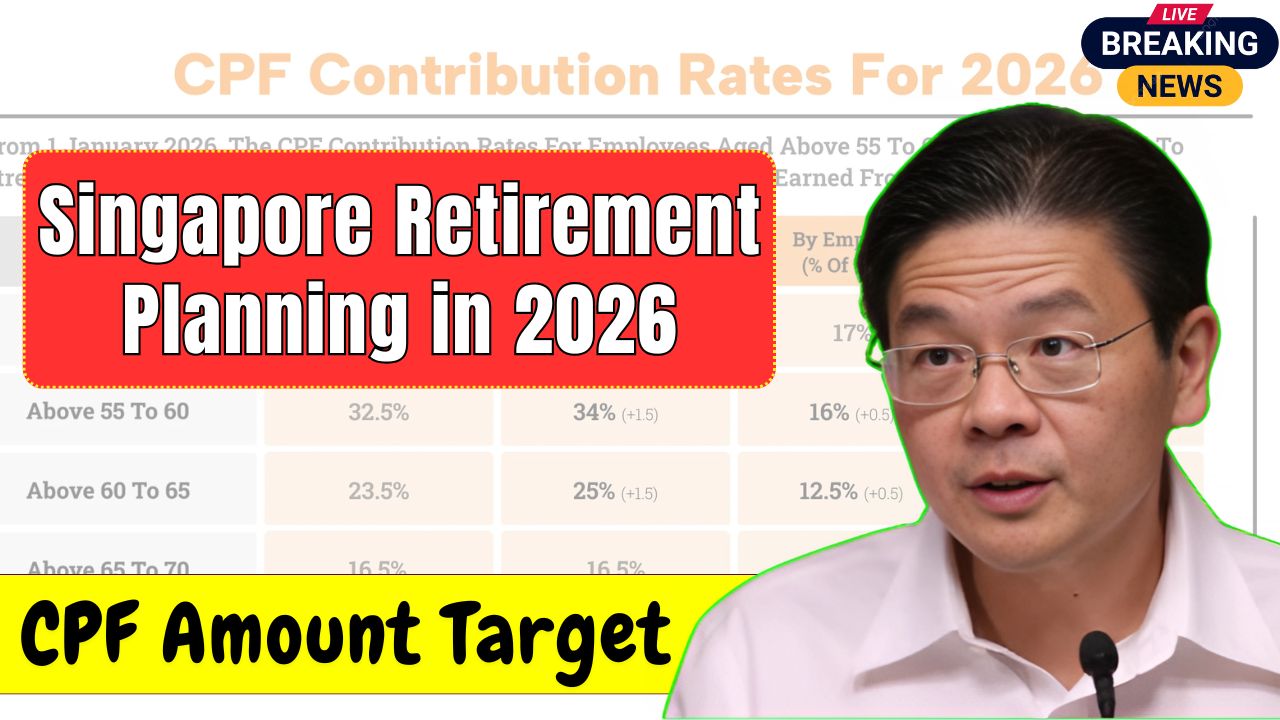

As Singapore moves into 2026, retirement planning has become more critical than ever. Rising living costs and longer life expectancy mean CPF savings must last longer, making it essential for individuals to understand how much retirement income they truly need.

How CPF Forms Your Retirement Income

CPF remains the backbone of retirement income for most Singaporeans. Contributions made during working years are channelled into retirement payouts after the payout age, providing a stable monthly income to support daily living expenses.

Estimated CPF Savings Needed for Retirement

The amount of CPF savings required depends on lifestyle expectations. A basic retirement may require lower CPF balances, while a more comfortable lifestyle demands higher savings to cover housing, healthcare, food, and personal expenses throughout retirement.

Role of CPF Retirement Account and Payouts

From age 55 onwards, CPF savings are consolidated into the Retirement Account. These funds are then used to generate monthly payouts from the payout age, ensuring retirees receive steady income instead of relying on lump sums.

Impact of Living Costs on Retirement Income

Inflation and healthcare costs play a major role in determining how much income retirees need. Expenses such as medical care, insurance, utilities, and daily essentials continue to rise, making adequate CPF savings crucial for financial security.

How Working Longer Can Improve CPF Retirement Income

Continuing to work beyond the traditional retirement age helps boost CPF balances through additional contributions. Higher savings translate into better monthly payouts, reducing financial stress in later years.

Conclusion

The Singapore retirement income outlook for 2026 highlights the importance of realistic CPF planning. By understanding expected expenses and building sufficient CPF savings early, individuals can secure a stable and comfortable retirement without financial uncertainty.